Loan Prepayment vs SIP Investment — Which Saves More?

Compare prepaying a loan vs investing in a SIP with the same amount. See which option builds more wealth.

Read the complete guideBetter Option

Invest in SIP

by ₹9,06,279 (78.8%) over 10 years

| Metric | Prepay Loan | Invest in SIP |

|---|---|---|

| Amount Used | ₹5,00,000 | ₹5,00,000 |

| Benefit | ₹2,43,914 saved | ₹11,50,193 earned |

| Net Outcome | ₹7,43,914 | ₹16,50,193 |

Assumption: Lump sum invested at 12% p.a. compounded monthly for 120 months. Prepayment reduces principal immediately. No tax implications modelled.

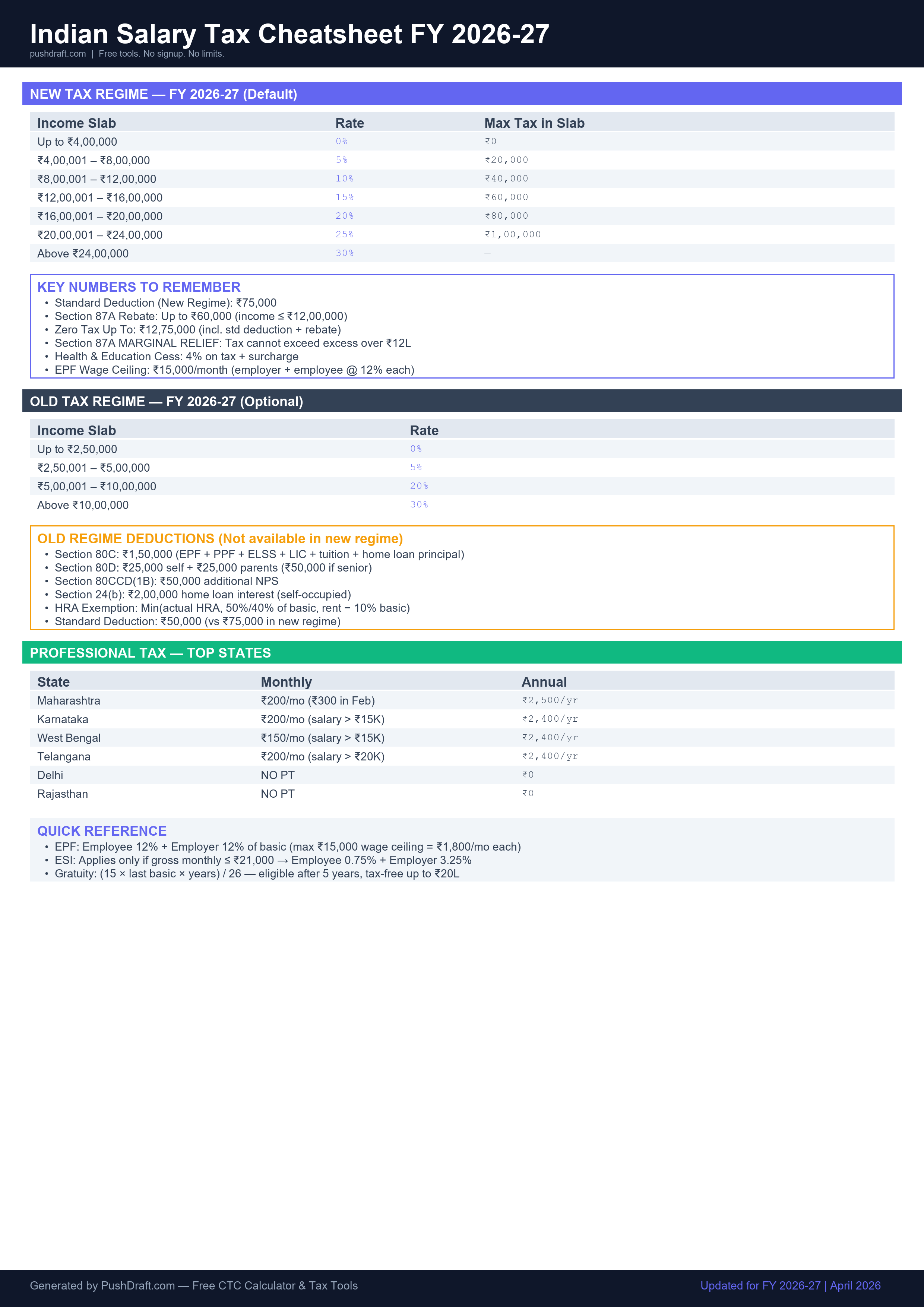

Free: Indian Salary Tax Cheatsheet 2026-27

New regime slabs, old regime deductions, PT by state — one page, print-ready.

{kind=link}

How to Use Loan vs SIP Calculator

-

Enter lump sum

The amount you have available to prepay or invest.

-

Enter loan details

Outstanding amount, interest rate, remaining tenure.

-

Enter SIP return

Expected annual return from equity mutual funds (12-15% typical).

-

Compare

See interest saved vs wealth gained and the verdict.

Related Tools

Frequently Asked Questions

Should I prepay my home loan or invest in SIP?

The math is simple: if your loan interest rate is higher than your expected investment return (post-tax), prepay the loan. For most people, home loans at 8-9% should be prepaid before investing, unless you are in the 30% tax bracket and claiming Section 24(b) deduction on interest.

PushDraft Weekly

Get weekly salary tips, tax updates, and new tools. Free, no spam, unsubscribe anytime.